Post-merger integration plan: cum eviți distrugerea valorii în primele 100 de zile după preluarea unei afaceri

Prețul a fost agreat. Contractul (SPA) a fost semnat. Comunicatul de presă este pregătit. Pentru mulți cumpărători și investitori, acesta pare momentul în care tranzacția s-a încheiat cu succes. În realitate, este începutul celei mai sensibile și riscante etape a întregului proces.

Conform analizelor publicate de Harvard Business Review, KPMG și Bain & Company între 70% și 90% dintre achiziții nu reușesc să genereze valoarea anticipată la momentul investiției. KPMG estimează că 83% dintre tranzacții nu reușesc dintre tranzacții nu livrează randamentele așteptate de acționari, iar Bain arată că doar aproximativ 30% ating obiectivele de sinergie asumate inițial. În majoritatea cazurilor, distrugerea de valoare nu este cauzată de o strategie greșită sau de un proces de due diligence insuficient. Problema apare după closing — prin deciziile întârziate, integrarea incoerentă sau lipsa unui plan operațional clar pentru primele luni post-tranzacție.

Primele 100 de zile după achiziție nu reprezintă o simplă perioadă administrativă de tranziție. Este intervalul în care premisele investiției sunt fie validate, fie încep să se erodeze. Angajații-cheie decid dacă rămân. Clienții își reevaluează relațiile comerciale. Procesele operaționale fie continuă stabil, fie încep să genereze tensiuni și disfuncționalități.

Fereastra pentru acțiuni decisive este scurtă și, de regulă, se închide mai rapid decât anticipează majoritatea cumpărătorilor.

Acest articol prezintă o abordare structurată a integrării post-achiziție în tranzacțiile mid-market, cu accent pe tiparele care generează pierdere de valoare și pe secvența de măsuri necesare pentru a le preveni.

De ce eșuează achizițiile în etapa de integrare

Înțelegerea cauzelor reale ale eșecului unei achiziții este mult mai valoroasă decât parcurgerea unei liste standard de verificare pentru integrarea post-achiziție. În tranzacțiile mid-market din Europa Centrală și de Est, și în majoritatea piețelor aceleași tipare care distrug valoare apar cu o regularitate remarcabilă.

Înainte de a analiza aceste tipare, este însă important să definim cu precizie ce înseamnă, în realitate, „eșecul” unei tranzacții. Statisticile frecvent citate privind rata ridicată de eșec în M&A sunt adesea utilizate fără a explica modul în care succesul sau eșecul sunt măsurate.

Cum este măsurat eșecul în M&A

O tranzacție se poate finaliza cu succes din punct de vedere juridic și procedural și, cu toate acestea, să nu genereze valoare pentru acționari. Atât literatura academică, cât și practica profesională utilizează mai multe metode complementare pentru evaluarea performanței unei achiziții.

Cea mai utilizată metodă în cercetarea academică este analiza performanței bursiere. În această abordare, o tranzacție este considerată distrugătoare de valoare atunci când acțiunile cumpărătorului înregistrează o performanță inferioară companiilor comparabile din același sector în perioada de unu până la trei ani după finalizarea achiziției. Premisa este simplă: dacă tranzacția a creat valoare, aceasta ar trebui să se reflecte în timp în performanța relativă a companiei pe piață.

O a doua metodă de evaluare se concentrează asupra realizării sinergiilor. Majoritatea achizițiilor sunt justificate prin economii de costuri, creșteri de venituri, eficiențe operaționale sau alte beneficii strategice. Atunci când aceste avantaje anticipate nu se materializează în primii doi-trei ani după closing, tranzacția este considerată că nu și-a îndeplinit teza investițională. Deși pragurile exacte diferă de la un studiu la altul, gradul de realizare a sinergiilor rămâne unul dintre cei mai utilizați indicatori ai succesului unei achiziții.

O a treia măsură, mai directă, este cesiunea activului achiziționat. Atunci când o companie cumpărată este vândută, separată sau cedată într-un interval relativ scurt — de regulă în primii cinci ani de la achiziție — acest lucru este adesea interpretat ca un semnal că fundamentul inițial al tranzacției nu a fost validat sau că integrarea nu a produs rezultatele așteptate. Desigur, astfel de decizii pot fi influențate și de factori independenți de integrare, precum schimbările în strategia de alocare a capitalului, reorganizarea portofoliului sau evoluțiile macroeconomice.

Rata de eșec de 70–90% frecvent citată în literatura de specialitate provine în principal din analiza tranzacțiilor realizate de companii listate, unde există suficiente date de piață pentru o evaluare relativ obiectivă a performanței post-achiziție.

În cazul companiilor private — contextul relevant pentru majoritatea tranzacțiilor mid-market din Europa Centrală și de Est — măsurarea este mai dificilă. Cu toate acestea, studiile care analizează gradul de realizare a sinergiilor, satisfacția investitorilor și performanța operațională post-achiziție indică concluzii similare: un număr semnificativ de tranzacții nu reușesc să genereze valoarea care a stat la baza deciziei de investiție.

Observația esențială este că aceste rezultate sunt rareori determinate de semnarea SPA-ului sau chiar de calitatea procesului de due diligence. În cele mai multe cazuri, ele sunt determinate de ceea ce se întâmplă — sau nu se întâmplă — în perioada de integrare care urmează după closing.

Ratele de eșec și experiența cumpărătorului

Ratele de eșec în tranzacțiile de M&A nu sunt uniforme. Ele variază semnificativ în funcție de tipul cumpărătorului, nivelul de experiență acumulat și disciplina aplicată atât în procesul de achiziție, cât și în etapa de integrare post-closing.

Un sondaj realizat în 2017 în rândul executivilor din companii și fonduri de private equity evidențiază diferențe relevante între cele două categorii de investitori.

În rândul cumpărătorilor strategici:

- 51% dintre respondenți au declarat că între 1% și 25% dintre achizițiile realizate în ultimii doi ani nu au generat randamentul investițional (ROI) anticipat,

- la celălalt capăt al spectrului, 6% au raportat că peste trei sferturi dintre tranzacțiile efectuate au eșuat în atingerea obiectivelor financiare asumate.

În cazul fondurilor de private equity, rezultatele au fost semnificativ mai bune:

- aproximativ 66% dintre respondenți au raportat rate de eșec cuprinse între 1% și 25%,

- iar doar 2% au indicat că peste 75% dintre investițiile realizate nu au atins randamentele așteptate:

Diferența nu este întâmplătoare. Investitorii de tip private equity operează, în general, cu procese investiționale mai structurate, mecanisme de guvernanță post-achiziție mai riguroase și sisteme de stimulare care leagă direct performanța echipei de crearea de valoare și de realizarea randamentului investițional.

Disciplina impusă de obiectivul de ROI influențează nu doar selecția țintelor de achiziție, ci și viteza și rigoarea cu care sunt implementate măsurile de integrare după closing. În schimb, programele de M&A corporative sunt adesea influențate de considerente strategice mai largi, de procese interne complexe de aprobare și de obiective care nu sunt întotdeauna corelate direct cu performanța financiară a unei tranzacții individuale. Acest lucru poate reduce nivelul de responsabilizare pentru realizarea beneficiilor anticipate și poate întârzia deciziile necesare în perioada post-achiziție.

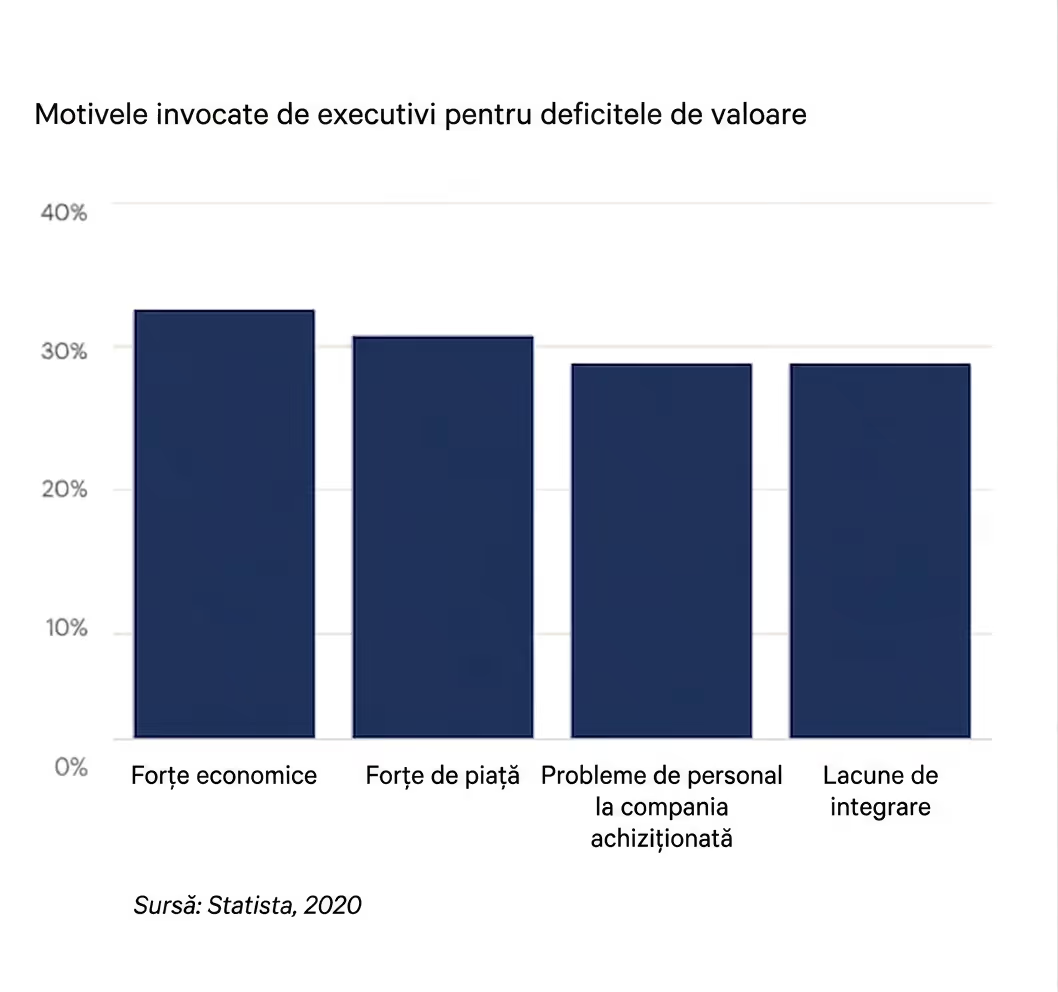

La fel de relevante sunt și motivele invocate de executivi pentru subperformanța tranzacțiilor. Forțele economice externe au fost identificate drept principalul factor, fiind menționate de 32% dintre respondenți. Acestea au fost urmate de schimbările în condițiile de piață, indicate de 30% dintre participanți.

Cu toate acestea, două dintre cele mai frecvente cauze raportate au fost direct legate de integrarea post-achiziție: problemele de personal și retenția talentelor în cadrul companiei achiziționate (28%), respectiv deficiențele procesului de integrare (28%).

Această distribuție este relevantă deoarece evidențiază o realitate frecvent întâlnită în tranzacțiile mid-market: deși factorii macroeconomici sunt imposibil de controlat, o parte semnificativă a distrugerii de valoare provine din elemente aflate direct sub controlul cumpărătorului. Retenția managementului-cheie, integrarea operațională, comunicarea internă și implementarea unui model de guvernanță eficient reprezintă variabile care pot fi gestionate și care influențează în mod direct probabilitatea ca o achiziție să își atingă obiectivele strategice.

Aceste statistici trebuie interpretate cu prudență, deoarece nu sunt defalcate pe sectoare sau pe tipuri de tranzacții, ceea ce limitează aplicabilitatea lor directă în evaluarea unui caz individual. Cu toate acestea, tiparul general este în concordanță cu ceea ce observăm în practică în tranzacțiile mid-market: achizițiile subperformează mai rar pentru că activul a fost supraevaluat și mult mai frecvent pentru că nu au fost create, înainte de semnare, condițiile necesare pentru generarea valorii după closing.

În multe cazuri, teza investițională este corectă, due diligence-ul este adecvat, iar prețul este justificabil. Problema apare atunci când integrarea este tratată ca o etapă secundară, în loc să fie planificată încă din faza de structurare a tranzacției. Dimensiunea tranzacției influențează semnificativ această dinamică. Spre deosebire de marile corporații, companiile din segmentul mid-market rareori dispun de echipe dedicate de integrare, metodologii formalizate sau resurse interne specializate în managementul schimbării. Ca urmare, multe tranzacții se finalizează fără infrastructura operațională necesară pentru executarea planului post-achiziție.

Rezultatul este că valoarea nu este distrusă prin erori strategice majore, ci prin acumularea unor probleme aparent minore: responsabilități neclare, procese nealiniate, întârzieri în luarea deciziilor, lipsa retenției personalului-cheie sau dificultăți în integrarea sistemelor și a fluxurilor operaționale. În segmentul mid-market, pierderea de valoare apare adesea prin neglijență operațională, mai degrabă decât prin factori de natură regulatorie sau structurală.

Sectorul de activitate influențează, la rândul său, probabilitatea de succes a unei achiziții.

Tranzacțiile din tehnologie înregistrează, în mod constant, unele dintre cele mai ridicate rate de eșec raportate. Estimările din industrie indică niveluri care se apropie de 90% în anumite categorii de tranzacții, în principal din cauza dificultății de integrare a echipelor și tehnologiilor, precum și a vitezei cu care avantajele competitive ale activelor achiziționate se pot eroda înainte ca integrarea să fie finalizată. În schimb, achizițiile din producție și industrie tind să fie mai stabile din perspectiva integrării. Activele sunt mai tangibile, relațiile comerciale sunt adesea mai predictibile, iar procesele operaționale sunt mai ușor de cartografiat și transferat. Totuși, aceste tranzacții vin cu propriul set de provocări: retenția forței de muncă specializate, transferul know-how-ului operațional, continuitatea producției și validarea ipotezelor privind productivitatea activelor și a echipamentelor.

În toate sectoarele, însă, concluzia rămâne aceeași: succesul unei achiziții este determinat mult mai puțin de semnarea tranzacției și mult mai mult de capacitatea cumpărătorului de a transforma teza investițională într-un plan de execuție concret după closing. Tranzacțiile care creează valoare sunt, de regulă, cele în care integrarea este planificată înainte de semnare, nu după aceasta.

Pattern-urile recurente ale eșecului în integrarea post-achiziție

Cauzele fundamentale ale eșecului tind să se concentreze în jurul acelorași deficiențe de execuție. Acestea nu sunt, de regulă, probleme de strategie sau de evaluare, ci erori de implementare care apar într-o perioadă relativ scurtă după closing și care, dacă nu sunt gestionate rapid, încep să erodeze valoarea tranzacției.

Pierderea talentului-cheie (Talent Flight)

Una dintre cele mai costisitoare forme de distrugere a valorii este pierderea angajaților-cheie în primele luni după achiziție. În anumite tranzacții, companiile achiziționate pot pierde până la 20% dintre persoanele esențiale pentru funcționarea afacerii. Aceștia sunt, de regulă, oamenii care dețin relațiile critice cu clienții, cunosc procesele operaționale și asigură continuitatea activității de zi cu zi.

Plecările rareori au loc brusc. Procesul începe încă din prima zi după anunțarea tranzacției, atunci când întrebările privind viitorul rolului lor, nivelul de autonomie, sistemul de remunerare sau intențiile noului proprietar rămân fără răspuns. Incertitudinea prelungită generează comportamente previzibile: angajații valoroși își actualizează CV-urile înainte ca managementul să realizeze că există o problemă.

Pierderea clienților (Customer Attrition)

În timp ce cumpărătorul se concentrează asupra integrării interne, concurenții se concentrează asupra clienților. În săptămânile care urmează anunțului unei tranzacții, conturile-cheie sunt adesea contactate de competitori care încearcă să exploateze incertitudinea creată de schimbarea proprietății.

Dacă nu există o comunicare rapidă și coordonată din partea noului proprietar, clienții încep să își reevalueze opțiunile. În special în companiile în care relațiile comerciale au fost construite în jurul fondatorului sau al unei echipe restrânse de management, pierderea încrederii poate conduce la diminuarea graduală a veniturilor care au stat la baza evaluării tranzacției.

Valoarea se pierde adesea înainte ca această pierdere să devină vizibilă în raportările financiare.

Paralizia decizională (Decision Paralysis)

Perioadele de integrare caracterizate prin responsabilități neclare reprezintă una dintre cele mai frecvente surse de ineficiență post-closing.

Două structuri organizaționale care coexistă simultan, două linii de raportare și două seturi de priorități care operează fără un model clar de guvernanță nu reprezintă o etapă de tranziție, ci un risc operațional.

În absența unor drepturi decizionale clar definite:

- managerii evită asumarea responsabilității;

- aprobările sunt întârziate;

- inițiativele comerciale sunt amânate;

- iar organizația își pierde ritmul operațional.

Fiecare zi în care nu este clar cine decide și cine răspunde pentru rezultate generează costuri care, deși dificil de cuantificat imediat, se acumulează rapid.

Supra-integrarea prea rapidă (Over-Integration)

O greșeală frecvent întâlnită este încercarea de a transforma compania achiziționată într-o copie a cumpărătorului înainte ca acesta să înțeleagă în detaliu ce anume a achiziționat. Migrarea accelerată a sistemelor IT, centralizarea proceselor de achiziții, modificarea structurilor organizaționale sau impunerea prematură a procedurilor corporative pot crea perturbări semnificative într-o afacere care funcționa eficient înainte de tranzacție.

În multe cazuri, cumpărătorul încearcă să captureze sinergiile prea devreme și ajunge să destabilizeze exact elementele care generau valoare. Integrarea eficientă presupune secvențiere și prioritizare, nu viteză maximă de execuție.

Pierderea tezei investiționale (Loss of the Deal Thesis)

Poate cea mai subtilă și mai periculoasă formă de eșec apare atunci când organizația pierde din vedere motivul pentru care tranzacția a fost realizată. În primele luni după closing, echipele de integrare sunt absorbite de probleme operaționale cotidiene: procese, sisteme, raportări, organigrame și aprobări. În acest context, factorii care au justificat investiția inițială pot înceta să mai primească atenția necesară.

Poate fi vorba despre:

- un segment strategic de clienți;

- o capacitate de producție specifică;

- o tehnologie;

- sau o echipă-cheie care reprezenta principalul activ al companiei achiziționate.

Elementul comun al tuturor acestor situații este că ele nu reprezintă, în esență, eșecuri de strategie. În majoritatea cazurilor, teza investițională rămâne validă. Problema apare la nivelul execuției.

Faza 0: înainte de Ziua 1

Cel mai puternic predictor al unei integrări reușite nu este calitatea planului elaborat după closing, ci faptul că acesta există înainte ca tranzacția să fie finalizată. Atunci când planificarea integrării începe în ziua semnării sau imediat după closing, primele săptămâni sunt consumate de întrebări care ar fi trebuit să aibă deja răspuns: cine ia deciziile, cine comunică, care sunt prioritățile și ce elemente ale afacerii trebuie protejate cu orice preț.

În tranzacțiile care generează valoare, integrarea începe înainte de Ziua 1. Până la momentul closing-ului, cumpărătorul ar trebui să fi definit cel puțin următoarele elemente:

- structura organizațională provizorie, mapată cel puțin pe primele două niveluri ierarhice;

- cadrul de comunicare pentru Ziua 1, inclusiv mesajele-cheie privind ceea ce se schimbă, ceea ce rămâne neschimbat și persoanele autorizate să comunice aceste informații;

- lista nominală a angajaților-cheie a căror retenție este critică pentru menținerea valorii tranzacției;

- modelul de guvernanță post-closing, construit în concordanță cu prevederile Shareholders’ Agreement (SHA), inclusiv drepturile decizionale, nivelurile de aprobare și mecanismele de escaladare;

- cei trei până la cinci factori esențiali de valoare pe care integrarea trebuie să îi protejeze și să îi consolideze.

În această etapă ar trebui să existe deja o structură formală de coordonare a integrării, de regulă sub forma unui Integration Committee (IC). Comitetul nu trebuie să fie o organizație extinsă și nici să gestioneze direct fiecare flux de lucru. Rolul său principal este de a asigura disciplina execuției: să coordoneze deciziile critice, să clarifice responsabilitățile, să elimine blocajele și să monitorizeze progresul. Un Integration Committee cu autoritate clară și mandat bine definit reduce semnificativ acest risc.

Obiectivul este ca, în dimineața Zilei 1, organizația să nu își pună întrebări fundamentale despre viitorul său. Aceste răspunsuri trebuie să existe deja.

Zilele 1–30: Stabilizare

Obiectivul primei luni după closing nu este transformarea organizației, ci stabilizarea acesteia. Primele 30 de zile reprezintă o perioadă de observare disciplinată, în care prioritatea este înțelegerea afacerii și protejarea activelor critice care au justificat achiziția.

Retenția personalului-cheie reprezintă prioritatea absolută a primei săptămâni.

Cumpărătorul trebuie să identifice rapid acei 10–20 de angajați a căror plecare ar avea un impact direct asupra operațiunilor, relațiilor comerciale sau know-how-ului organizațional. În multe cazuri, aceștia nu sunt neapărat managerii cei mai seniori, ci persoanele care dețin cunoștințe critice, relații comerciale esențiale sau expertiză dificil de înlocuit.

Procesul decizional al acestor angajați începe din Ziua 1. Dacă nu primesc claritate privind rolul lor în noua organizație, perspectivele de dezvoltare și intențiile noului proprietar, își vor căuta singuri alternative. Din acest motiv, acordurile de retenție, clarificarea responsabilităților și implicarea directă a managementului cumpărătorului trebuie implementate în primele 7–10 zile după closing, nu după primele luni de integrare.

Continuitatea relațiilor cu clienții

În paralel, continuitatea bazei de clienți trebuie tratată ca o prioritate strategică. Conducerea cumpărătorului ar trebui să contacteze personal principalii clienți ai companiei achiziționate în prima săptămână după finalizarea tranzacției. Obiectivul nu este vânzarea sau renegocierea relației comerciale, ci transmiterea unui mesaj clar de stabilitate.

Mesajul trebuie să fie simplu și consecvent:

- activitatea continuă fără întreruperi;

- angajamentele comerciale existente sunt respectate;

- echipa și persoanele de contact rămân disponibile;

- iar tranzacția creează premise pentru dezvoltarea viitoare a relației.

Acest lucru este esențial deoarece concurenții nu așteaptă. În majoritatea piețelor, aceștia vor contacta clienții-cheie imediat după anunțarea tranzacției, încercând să exploateze orice semnal de incertitudine.

Stabilitate operațională

Una dintre cele mai frecvente greșeli în această etapă este confundarea integrării cu transformarea. Prima lună nu este momentul pentru reorganizări majore, restructurări sau inițiative agresive de optimizare. Este momentul în care cumpărătorul trebuie să înțeleagă cum funcționează afacerea înainte de a încerca să o schimbe.

Indicatorii de succes sunt simpli:

- salariile sunt plătite la timp;

- comenzile sunt procesate normal;

- livrările sunt efectuate fără întârzieri;

- sistemele funcționează;

- iar clienții nu observă perturbări semnificative.

Claritate de guvernanță

Până la finalul primei luni, fiecare angajat trebuie să știe cui raportează, cine îi evaluează performanța și cine are autoritatea de a lua decizii relevante pentru activitatea sa.

Ambiguitatea organizațională nu se rezolvă în timp. Dimpotrivă, tinde să se amplifice. Atunci când responsabilitățile și liniile de raportare nu sunt clar definite, organizația începe să încetinească: deciziile sunt amânate, inițiativele sunt blocate, iar managerii evită asumarea responsabilității. De aceea, unul dintre obiectivele esențiale ale primelor 30 de zile este eliminarea incertitudinii privind modelul de guvernanță și comunicarea clară a structurii decizionale post-closing.

Zilele 31–80: Aliniere și capturarea valorii

După ce riscurile imediate asociate perioadei post-closing au fost stabilizate, integrarea intră într-o nouă etapă. Dacă primele 30 de zile au fost dedicate protejării valorii existente, intervalul dintre zilele 31 și 80 are ca obiectiv începerea capturării valorii anticipate în teza investițională.

Quick Wins: construirea credibilității prin rezultate

Primele beneficii rezultate din tranzacție trebuie să fie vizibile relativ rapid. Așa-numitele quick wins au două funcții esențiale. În primul rând, generează rezultate financiare timpurii care validează rațiunea economică a achiziției. În al doilea rând, construiesc credibilitate internă pentru procesul de integrare și demonstrează că schimbarea produce beneficii concrete.

În tranzacțiile mid-market, exemplele tipice includ:

- consolidarea achizițiilor și renegocierea contractelor cu furnizorii pe baza volumelor combinate;

- eliminarea furnizorilor sau contractelor redundante;

- valorificarea oportunităților evidente de cross-selling către clienții existenți;

- optimizarea unor costuri administrative duplicate.

Gestionarea sinergiilor ca proces financiar

Una dintre cele mai frecvente greșeli în integrarea post-achiziție este tratarea sinergiilor ca simple obiective de proiect. În realitate, sinergiile trebuie gestionate cu aceeași disciplină aplicată indicatorilor financiari.

Fiecare sinergie identificată în modelul investițional ar trebui să aibă:

- un responsabil clar desemnat;

- o bază de referință (baseline);

- o țintă cuantificabilă;

- un calendar de implementare;

- și un mecanism de raportare.

Experiența arată că sinergiile care nu sunt monitorizate sistematic tind să nu se materializeze. Nu pentru că sunt imposibil de realizat, ci pentru că organizația își îndreaptă atenția către alte priorități operaționale.

Cultura organizațională ca flux de lucru, nu ca inițiativă de HR

Diferențele culturale dintre cele două organizații devin vizibile mult mai repede decât majoritatea cumpărătorilor anticipează. În câteva săptămâni apar întrebări fundamentale:

- Cum sunt luate deciziile?

- Cum este evaluată performanța?

- Cum sunt gestionate conflictele?

- Cât autonomie au managerii?

Apariția întrebărilor nu reprezintă un semn de eșec. Dimpotrivă, este un fenomen natural în orice integrare. Problema apare atunci când ele sunt ignorate. Cultura se aliniază prin modul în care organizația lucrează împreună, nu prin modul în care vorbește despre integrare.

Planificarea integrării sistemelor

În această etapă, prioritatea este înțelegerea și planificarea, nu implementarea. Înainte de orice migrare, cumpărătorul trebuie să construiască o imagine completă a infrastructurii operaționale și tehnologice a companiei achiziționate:

- ce sisteme există;

- care sunt critice pentru funcționarea afacerii;

- unde există redundanțe;

- care sunt dependențele dintre aplicații și procese;

- și în ce ordine ar trebui realizată integrarea.

Multe dintre perturbările operaționale observate în lunile trei și patru după closing au o cauză comună: migrarea prematură a sistemelor înainte ca organizația să înțeleagă pe deplin modul în care acestea susțin activitatea curentă. Integrarea sistemelor nu este un exercițiu tehnic. Este un exercițiu de continuitate operațională.

Obiectivul: organizația ar trebui să fi demonstrat primele rezultate concrete ale tranzacției, să fi început capturarea sinergiilor cu risc redus, să fi identificat și gestionat principalele puncte de tensiune culturală și să dețină un plan clar pentru integrarea funcțională și tehnologică.

Zilele 81–100: Execuție și asigurarea valorii

Accentul nu mai este pus pe stabilizare sau pe capturarea primelor sinergii, ci pe validarea tezei investiționale și pe pregătirea organizației pentru următoarea fază a dezvoltării. Aceasta este etapa în care succesul integrării începe să fie măsurat prin rezultate, nu prin activități.

Măsurarea performanței

Unul dintre cele mai frecvente riscuri în această fază este supraîncărcarea organizației cu indicatori și rapoarte care consumă timp fără să ofere claritate. În practică, cele mai eficiente procese de integrare urmăresc un număr limitat de indicatori-cheie, direct corelați cu teza investițională a tranzacției.

În mod obișnuit, aceștia includ:

- rata de retenție a angajaților-cheie;

- retenția clienților raportată la baza existentă înainte de closing;

- gradul de realizare a sinergiilor față de planul inițial;

- stabilitatea operațională și continuitatea livrării;

- veniturile generate din inițiativele de cross-selling și dezvoltare comercială.

Acești indicatori nu ar trebui monitorizați exclusiv la nivel operațional. Ei trebuie raportați și evaluați periodic de către steering committee-ul tranzacției, deoarece reprezintă cei mai relevanți indicatori ai progresului în realizarea valorii investiției.

Planul de integrare pe 12–18 luni

Pe măsură ce perioada inițială de integrare se apropie de final, rolul Integration Committee-ului începe să se schimbe. Obiectivul nu mai este coordonarea activităților zilnice, ci predarea către management a unui plan clar și credibil pentru următoarele 12–18 luni.

O atenție specială trebuie acordată dependențelor care continuă să existe după closing. În multe tranzacții, acestea sunt gestionate prin intermediul unor TSA-uri (Transition Services Agreements), prin care vânzătorul continuă să furnizeze anumite servicii pentru o perioadă limitată de timp. Aceste servicii pot include suport IT, funcții financiare, servicii administrative, operațiuni logistice sau alte activități necesare pentru continuitatea afacerii.

Un TSA bine structurat reprezintă un instrument valoros de reducere a riscului operațional. Cu toate acestea, eficiența sa depinde de existența unei strategii clare de ieșire.

Fiecare serviciu furnizat în baza unui TSA ar trebui să aibă:

- un termen clar de încetare;

- responsabilități bine definite;

- o structură de cost transparentă;

- și un plan de transfer către cumpărător.

În absența acestor elemente, dependențele temporare tind să devină permanente.

În practică, multe companii descoperă că serviciile care trebuiau înlocuite în șase luni sunt încă utilizate după doi ani, generând costuri suplimentare și limitând autonomia organizației.

Considerații specifice integrării post-achiziție în Ungaria

Deși principiile fundamentale ale integrării post-achiziție sunt similare în majoritatea jurisdicțiilor, anumite particularități juridice, fiscale și culturale ale pieței maghiare pot influențai succesul procesului de integrare. În tranzacțiile mid-market, aceste aspecte sunt adesea subestimate de cumpărătorii internaționali.

Dreptul muncii și transferul angajaților

Transferurile de personal, reorganizările și modificările structurii organizaționale pot declanșa obligații de informare și consultare în temeiul legislației muncii din Ungaria, în special atunci când compania dispune de consilii ale angajaților (works councils) sau este parte la acorduri colective de muncă.

În astfel de situații, cumpărătorul trebuie să se asigure că:

- angajații sunt informați în termen util cu privire la transferul afacerii;

- obligațiile de consultare sunt respectate înainte de implementarea măsurilor relevante;

- modificările organizaționale sunt compatibile cu drepturile și obligațiile existente în cadrul raporturilor de muncă.

În practică, restructurările accelerate înainte de finalizarea procedurilor obligatorii de consultare generează adesea expuneri juridice și litigii care depășesc beneficiile operaționale urmărite.

Din acest motiv, analiza structurii forței de muncă și a obligațiilor asociate ar trebui să înceapă în etapa de due diligence și să fie integrată în planificarea post-closing, nu tratată ca o problemă administrativă ulterioară.

Înregistrarea modificărilor de guvernanță

După finalizarea tranzacției, modificările privind administratorii, reprezentanții legali, semnatarii autorizați și documentele de guvernanță corporativă trebuie înregistrate la instanța competentă de registru comercial din Ungaria. Până la finalizarea acestor formalități, anumite aspecte legate de reprezentarea companiei și exercitarea dreptului de semnătură pot deveni sensibile din punct de vedere operațional.

În această perioadă de tranziție este esențial ca:

- drepturile de reprezentare să fie clar documentate;

- competențele de aprobare să fie comunicate intern;

- iar deciziile semnificative să fie coordonate împreună cu consilierii juridici locali.

Cumpărătorii care se confruntă pentru prima dată cu aceste proceduri tind să subestimeze impactul pe care o structură de guvernanță aflată în tranziție îl poate avea asupra activității.

Cultura decizională și integrarea managementului

În segmentul mid-market din Ungaria, procesele decizionale tind să fie mai ierarhice decât se așteaptă mulți cumpărători din Europa de Vest sau din organizațiile multinaționale. În lipsa unei autorități clar definite, deciziile sunt adesea amânate, iar organizația preferă să aștepte clarificări înainte de a acționa.

Din acest motiv, definirea și comunicarea timpurie a:

- structurii organizaționale;

- responsabilităților manageriale;

- și drepturilor decizionale

nu reprezintă doar o bună practică managerială, ci o condiție esențială pentru menținerea vitezei de execuție după closing.

La fel de importantă este și gestionarea echipei de management existente. În multe tranzacții, cumpărătorii sunt tentați să implementeze rapid propriile structuri și să reducă rolul conducerii locale. În absența unui plan de succesiune credibil și a unor mecanisme clare de transfer al responsabilităților, această abordare poate genera rezistență internă semnificativă.

Vizibilitatea și implicarea echipei de conducere existente în primele luni după achiziție reprezintă, prin urmare, un factor critic de succes.

Fiscalitate și conformitate

Deși regimul fiscal corporativ din Ungaria este considerat unul dintre cele mai competitive din Europa, perioada imediat următoare closing-ului necesită o atenție deosebită din perspectiva conformității fiscale și financiare.

În practică, cele mai frecvente provocări apar în legătură cu:

- politicile de prețuri de transfer;

- tranzacțiile intra-grup;

- alinierea procedurilor de raportare financiară;

- obligațiile de înregistrare și raportare în scopuri de TVA;

- integrarea funcțiilor financiare și de controlling.

Cumpărătorii care finalizează tranzacția, dar amână integrarea proceselor financiare și fiscale, descoperă adesea dificultăți la prima închidere lunară sau trimestrială post-achiziție. Din acest motiv, armonizarea procedurilor financiare, fiscale și de raportare ar trebui să fie tratată ca o prioritate a primelor 100 de zile și nu ca un proiect administrativ secundar..

Considerații specifice integrării post-achiziție în România

Deși principiile fundamentale ale integrării post-achiziție sunt similare în majoritatea jurisdicțiilor, România prezintă o serie de particularități juridice, de reglementare și culturale care influențează direct ritmul și succesul procesului de integrare.

Guvernanță corporativă și Registrul Comerțului

După finalizarea tranzacției, modificările privind administratorii, reprezentanții legali și documentele constitutive ale societății trebuie înregistrate formal la Registrul Comerțului înainte ca acestea să producă efecte juridice depline. În cazul investitorilor străini, procesul poate implica documentație suplimentară, inclusiv legalizări, apostilări sau traduceri autorizate, ceea ce poate prelungi calendarul de implementare.

Până la finalizarea înregistrărilor, anumite aspecte privind reprezentarea companiei și exercitarea autorității decizionale pot deveni sensibile din punct de vedere operațional.

Din acest motiv, este esențial ca:

- drepturile de reprezentare să fie clar documentate;

- fluxurile de aprobare să fie definite și comunicate;

- iar deciziile critice să fie coordonate împreună cu avocații locali.

Acest aspect este frecvent subestimat. Cumpărătorii care tratează actualizarea Registrului Comerțului ca pe o simplă formalitate administrativă descoperă uneori că anumite acțiuni operaționale nu pot fi implementate cu viteza anticipată.

Transferul angajaților și conformitatea cu Codul Muncii

Transferul personalului este reglementat atât de Codul muncii, cât și de Legea nr. 67/2006 privind protecția drepturilor salariaților în cazul transferului de întreprinderi.

În practică, cumpărătorul trebuie să asigure:

- transferul contractelor individuale de muncă în condițiile existente;

- informarea și, după caz, consultarea angajaților conform cerințelor legale;

- respectarea procedurilor aplicabile în cazul restructurărilor sau concedierilor colective.

Una dintre cele mai frecvente greșeli în perioada imediat următoare closing-ului este accelerarea restructurărilor înainte de finalizarea proceselor de transfer și consultare.

Pe termen scurt, această abordare poate părea eficientă. Pe termen lung, însă, generează exact riscul pe care cumpărătorul încearcă să îl evite: pierderea personalului-cheie.

În companiile mid-market din România, reacția la percepția de instabilitate este rareori una conflictuală. Mult mai frecvent, angajații valoroși aleg să plece discret înainte ca organizația să realizeze amploarea problemei.

Cerințe de reglementare specifice sectorului

În sectoarele reglementate, integrarea trebuie coordonată atent cu obligațiile de notificare și autorizare impuse de autoritățile competente. În funcție de industrie și structura tranzacției, instituții precum ANRE, ASF sau ANCOM pot solicita notificări post-achiziție, aprobări privind schimbarea controlului sau actualizarea anumitor licențe și autorizații.

Chiar și în cazul unui share deal, unde entitatea operațională rămâne aceeași, schimbarea controlului poate declanșa obligații suplimentare de conformitate.

Aceste cerințe nu reprezintă formalități administrative, ci condiții necesare pentru continuarea neîntreruptă a activității. Nerespectarea lor poate conduce la sancțiuni, restricții operaționale sau, în cazuri extreme, la suspendarea anumitor activități.

GDPR și conformitatea privind datele

În ultimii ani, conformitatea privind protecția datelor a devenit o componentă importantă a integrării post-achiziție. Atunci când tranzacția implică baze de date cu clienți, informații despre angajați sau transferuri internaționale de date, cadrul GDPR trebuie analizat încă din etapa de due diligence și validat înainte de Ziua 1.

În funcție de structura tranzacției, pot fi necesare:

- actualizarea notelor de informare privind prelucrarea datelor;

- revizuirea acordurilor de prelucrare a datelor;

- actualizarea mecanismelor de transfer internațional;

- implementarea unor măsuri suplimentare de conformitate.

Cultura organizațională și comunicarea

În România, integrarea este influențată într-o măsură semnificativă de relațiile interpersonale și de încrederea construită la nivelul echipelor. Comunicarea exclusiv prin e-mailuri, prezentări sau notificări formale este rareori suficientă pentru a crea sentimentul de stabilitate necesar după o schimbare de proprietate.

Experiența arată că întâlnirile directe, sesiunile de tip town hall și prezența fizică a conducerii în organizație au un impact disproporționat de mare asupra retenției și implicării angajaților.

Mesajele trebuie să fie clare și consecvente:

- ce se schimbă;

- ce rămâne neschimbat;

- și care este direcția strategică a organizației.

La fel ca în alte piețe din Europa Centrală și de Est, vizibilitatea managementului local reprezintă un factor esențial de stabilitate. Capacitatea cumpărătorului de a păstra echipa de management existentă într-un rol relevant în primele 90 de zile este adesea unul dintre cei mai buni indicatori ai succesului integrării.

Clauza de neconcurență și tranziția proprietarului

În majoritatea tranzacțiilor mid-market din România, compania este puternic asociată cu fondatorul sau cu proprietarul său. Din acest motiv, comportamentul vânzătorului după closing devine o variabilă importantă a procesului de integrare.

Un fost proprietar care păstrează influență asupra angajaților-cheie, continuă să interacționeze informal cu clienții sau sprijină indirect activități concurente poate afecta semnificativ retenția personalului și stabilitatea comercială.

O clauză de neconcurență eficientă trebuie să definească în mod clar:

- activitățile restricționate;

- aria geografică relevantă;

- durata obligației;

- și mecanismele de protecție aplicabile.

În tranzacțiile mid-market din România și Ungaria, perioadele de doi până la trei ani sunt frecvent întâlnite atunci când acestea sunt proporționale cu valoarea fondului de comerț transferat.

Riscul de integrare este o categorie de due diligence

Cumpărătorii cu experiență nu tratează integrarea ca pe o activitate care începe după semnarea SPA-ului. Ei utilizează procesul de due diligence pentru a identifica factorii care vor determina succesul integrării: angajații critici, relațiile comerciale dependente de fondator, sistemele care necesită înlocuire, dependențele față de vânzător și constrângerile operaționale care vor continua după closing. O listă de verificare a integrării construită după finalizarea tranzacției este, prin definiție, un instrument reactiv.

Construită în timpul due diligence-ului, aceasta devine un instrument strategic care influențează structura tranzacției, mecanismele de ajustare a prețului, obligațiile post-closing și termenii eventualelor Transition Services Agreements (TSA).

În majoritatea cazurilor, diferența dintre o tranzacție care își realizează teza investițională și una care începe să distrugă valoare în primele 100 de zile nu este dată de strategie.

Concluzie

Primele 100 de zile după closing nu reprezintă o simplă perioadă de tranziție. Ele sunt intervalul în care teza investițională a tranzacției începe să fie validată sau, dimpotrivă, să se erodeze.

Cele mai multe achiziții nu subperformează din cauza unei strategii greșite sau a unui proces de due diligence insuficient. Problemele apar, de regulă, atunci când riscurile previzibile de integrare — pierderea angajaților-cheie, incertitudinea clienților, lipsa clarității decizionale sau întârzierile în capturarea sinergiilor — nu sunt identificate și gestionate suficient de devreme.

Niciunul dintre tiparele de eșec prezentate în acest articol nu este inevitabil. Toate sunt previzibile și, în mare măsură, prevenibile. Nu prin structuri complexe de integrare sau echipe numeroase, ci prin planificare riguroasă, responsabilități clar definite și decizii luate înainte de closing. Cumpărătorii care obțin rezultate constant superioare tratează integrarea ca pe o disciplină care începe în etapa de due diligence și continuă mult după semnarea tranzacției. Ei identifică riscurile de retenție înainte de closing, înțeleg dependențele față de fondator, cartografiază relațiile critice cu clienții și definesc modelul de guvernanță înainte de Ziua 1. Sinergiile sunt urmărite ca obiective financiare, nu ca simple activități de proiect.

Acest lucru este cu atât mai important în tranzacțiile mid-market din Europa Centrală și de Est, unde dependența de proprietar este adesea mai ridicată, procesele sunt mai puțin instituționalizate, iar încrederea clienților și a angajaților este mai greu de reconstruit odată pierdută. În astfel de situații, efectele unei integrări deficitare se propagă rapid: pierderea talentelor conduce la pierderea clienților, care la rândul său generează instabilitate operațională și reduce capacitatea de a captura valoarea anticipată.

În același timp, particularitățile juridice și de reglementare din România și Ungaria nu reprezintă simple formalități administrative. Acestea influențează direct secvența acțiunilor, calendarul implementării și capacitatea cumpărătorului de a executa planul de integrare fără întreruperi. Înțelegerea lor corectă nu este doar o chestiune de conformitate, ci o condiție necesară pentru succesul tranzacției.

La Ferdinand Investment Partners asistăm investitori strategici, antreprenori și fonduri de private equity în tranzacții și proiecte de integrare post-achiziție în România, Ungaria și în regiunea mai largă a Europei Centrale și de Est. Dacă analizați o oportunitate de achiziție și doriți să evaluați critic nivelul de pregătire pentru integrare înainte de closing, vă putem ajuta - fie printr-un apel, fie printr-un simplu mesaj pentru a începe discuția.

Întrebări frecvente despre planul de integrare post-achiziție

Ce este un plan de integrare post-achiziție și ce ar trebui să includă?

Un plan de integrare post-achiziție reprezintă cadrul prin care cumpărătorul gestionează tranziția de la closing la capturarea valorii anticipate prin tranzacție. Acesta ar trebui să acopere guvernanța și drepturile de decizie, retenția angajaților-cheie, comunicarea cu clienții, continuitatea operațională, monitorizarea sinergiilor și gestionarea eventualelor TSA-uri. În tranzacțiile cross-border, planul trebuie adaptat și la cerințele juridice și de reglementare ale jurisdicției relevante.

Ce este un Transition Services Agreement (TSA)?

Un TSA este acordul prin care vânzătorul continuă să furnizeze anumite servicii operaționale pentru o perioadă limitată după closing. Aceste servicii pot include suport IT, salarizare, contabilitate, logistică sau alte funcții esențiale pentru continuitatea afacerii. Un TSA eficient definește clar serviciile, costurile, durata și calendarul de ieșire pentru fiecare activitate transferată.

Cum poate fi redactată o clauză de neconcurență executorie?

O clauză de neconcurență trebuie să fie specifică, proporțională și adaptată activității transferate. Aceasta ar trebui să definească în mod clar activitățile restricționate, aria geografică și durata obligației. În tranzacțiile mid-market din România și Ungaria, perioadele de doi până la trei ani sunt frecvent întâlnite, însă caracterul executoriu depinde întotdeauna de circumstanțele concrete și de legislația aplicabilă.

Cum poate fi evaluată dependența unei companii de proprietar?

Analiza urmărește în ce măsură relațiile cu clienții, furnizorii, procesele operaționale și know-how-ul organizațional depind de implicarea directă a fondatorului. Cu cât aceste dependențe sunt mai mari, cu atât tranziția trebuie planificată mai atent, inclusiv prin mecanisme de earn-out, acorduri de consultanță și clauze de neconcurență.

Care sunt cele mai frecvente riscuri de integrare?

Cele mai întâlnite riscuri sunt pierderea angajaților-cheie, pierderea clienților, lipsa clarității decizionale, perturbările operaționale generate de schimbări premature și neatingerea sinergiilor estimate. Majoritatea acestor riscuri pot fi identificate și gestionate înainte de closing.

Care sunt principalele diferențe între integrarea în România și Ungaria?

Ambele jurisdicții impun formalități privind transferul angajaților și actualizarea guvernanței corporative, însă există diferențe importante la nivel de reglementare și practică. În Ungaria, consultarea structurilor de reprezentare a angajaților poate influența calendarul restructurărilor. În România, actualizările la Registrul Comerțului și obligațiile specifice sectoarelor reglementate necesită o atenție deosebită. În ambele piețe, comunicarea directă și menținerea vizibilității managementului local reprezintă factori esențiali pentru succesul integrării.